Foreclosure rate rises 23% in Sarasota and Manatee counties.

Foreclosure rate rises 23% in Sarasota and Manatee counties.

More Southwest Florida homeowners are struggling to pay their mortgages.

The number of residential properties with a foreclosure filing rose 23% as of mid-year in the Sarasota-Manatee region, according to a new report from real estate researcher ATTOM Data Solutions.

While foreclosures nationwide were down during the first half of 2019, the local increase was not that unusual. Foreclosure starts were higher in four out of 10 metros across the country. A total of 1,277 residential properties, or one in every 327 homes in the Sarasota-Manatee area, were in some stage of distress. That represents 0.31% of the housing units in the region.

But those filings – default notices, scheduled auctions and bank repossessions – are nearly 90% off their peak levels reached in 2008-2010 during the depths of the housing crash.

Florida posted the nation’s fourth-highest foreclosure rate at 0.39%, with the year-over-year increase the second highest in the U.S. The national foreclosure rate was 0.22%.

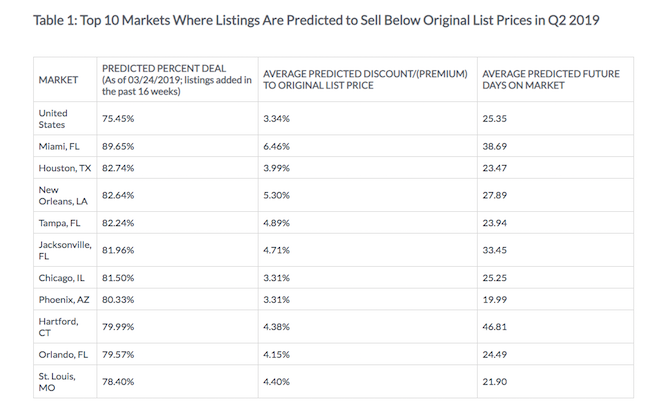

“Our mid-year 2019 foreclosure activity helps to show an overall view on how foreclosure activity is trending downward,” said Todd Teta, chief product officer at ATTOM. “Of course, you still have pockets across the nation where foreclosure activity is seeing some flare-ups. Foreclosure starts is a good indication of markets to watch. For instance, in looking at the largest markets across the nation with the greatest annual increase in foreclosure starts, four out of the five markets were in Florida.”

Charlotte County reported 379 filings, or one in every 271 housing units. That was 19% higher than the year before.

Last year foreclosure activity in Sarasota-Manatee receded to its lowest level since 2006, and has now held for several years at what analysts consider a normal volume of troubled homeowners. Filings have tumbled from the days when the region posted one of the top foreclosure rates in the nation.

Florida reported the third-longest average foreclosure timelines, from filing to completion, at 1,073 days. The national average was 716 days.

Fifth Third boosts pay

Fifth Third Bancorp is bumping the minimum wage it pays to employees to $18 per hour.

An estimated 4,900 workers will get the $3 hourly raise starting Oct. 28. Fifth Third, the sixth-largest bank in the Sarasota-Manatee metro area, said the increase recognizes the contributions of employees in driving the success of the bank and its customers.

“A competitive compensation and benefits package is essential to our ability to attract and retain the industry’s best and brightest,” said chairman/president/CEO Greg D. Carmichael.

The raise will bring those workers about $500 more per month on a pre-tax basis. It will cost the bank about $15 million a year.

The Cincinnati-based bank raised its minimum wage from $12 to $15 in January 2018, which it says contributed to a 16% annual reduction in employee turnover last year among workers most affected by that wage. The higher wage primarily impacts employees in retail branches and operations support functions such as customer contact centers. It will not be paid to employees who work on a commissioned basis, whose earnings typically run above $18 per hour.

Herald-Tribune August 2019

After wild swings before and after the economic downturn, home prices are inching closer to their pre-recession peaks in the Sarasota-Manatee County region.

After wild swings before and after the economic downturn, home prices are inching closer to their pre-recession peaks in the Sarasota-Manatee County region.

In a reverse of headlines – Regional Home Prices Lag. Home prices continue to rise in Southwest Florida, but not as fast as in the state or nationally.

In a reverse of headlines – Regional Home Prices Lag. Home prices continue to rise in Southwest Florida, but not as fast as in the state or nationally. Florida housing outlook tops big-picture on the national scene

Florida housing outlook tops big-picture on the national scene Home-price gains in Sarasota and Manatee County lagged behind the state and nation in October.

Home-price gains in Sarasota and Manatee County lagged behind the state and nation in October. Southwest Florida — the Sarasota metro area in particular — has a reputation for its wealth of gold-plated residences. The latest Luxury Home Index from realtor.com validates that celebrity status, or, from another viewpoint, notoriety.

Southwest Florida — the Sarasota metro area in particular — has a reputation for its wealth of gold-plated residences. The latest Luxury Home Index from realtor.com validates that celebrity status, or, from another viewpoint, notoriety. Projects East of Trail are poised to begin construction soon.

Projects East of Trail are poised to begin construction soon.